- The Federal Reserve kept interest rates unchanged after their latest meeting

- Some analysts think economic indicators show Fed rate hikes aren’t working

- A severe recession may be necessary to break the hold of inflation on the economy

Fed Pauses Rate Hikes

After its most recent meeting, the Federal Reserve choose not to raise interest rates again. Instead, they are taking a wait and see approach to observe the impact of previous rate hikes. While some may be happy to see a pause, others see a potential mistake.

1

1

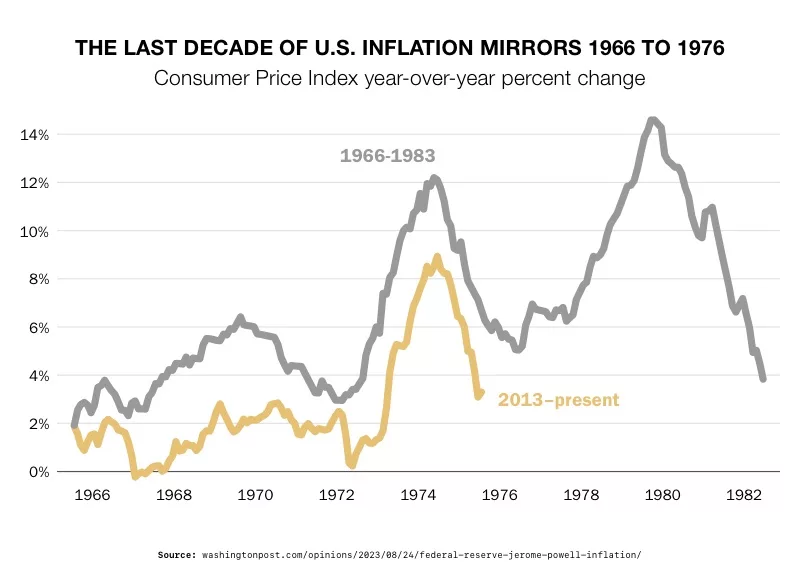

The facts on the ground show that the Fed’s policy isn’t working as anticipated. The economy is still too strong, and inflation is too high, even with 5.25 percentage points of rate hikes since March 2022. While the current 3.4% PCE rate (a measure of inflation that reflects changes in the prices of goods and services purchased by households for consumption) is better than the previous 7%, it is still far from 2%.2

In addition, the labor market is too resilient to reach the 2% inflation objective. The ratio of unfilled jobs to unemployed workers is well above the 1-to-1 ratio that Fed Chair Powell considers necessary.

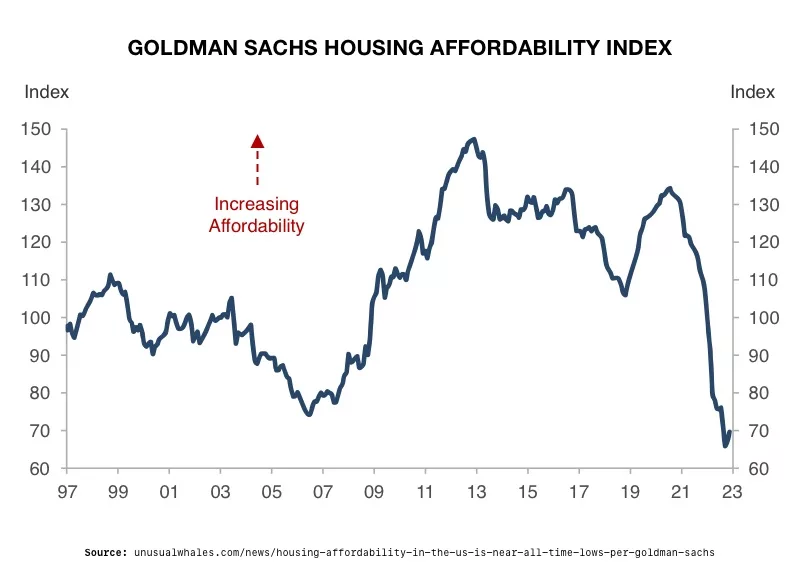

Despite wages going up, overall inflation has outpaced wage growth. Consumers have been making up the difference with excess savings boosted by Covid relief. But those savings are running out. Consumers are cutting back and sinking into debt to stay above water. To make matters worse, spiking oil prices are eroding purchasing power and putting the brakes on the American economy.

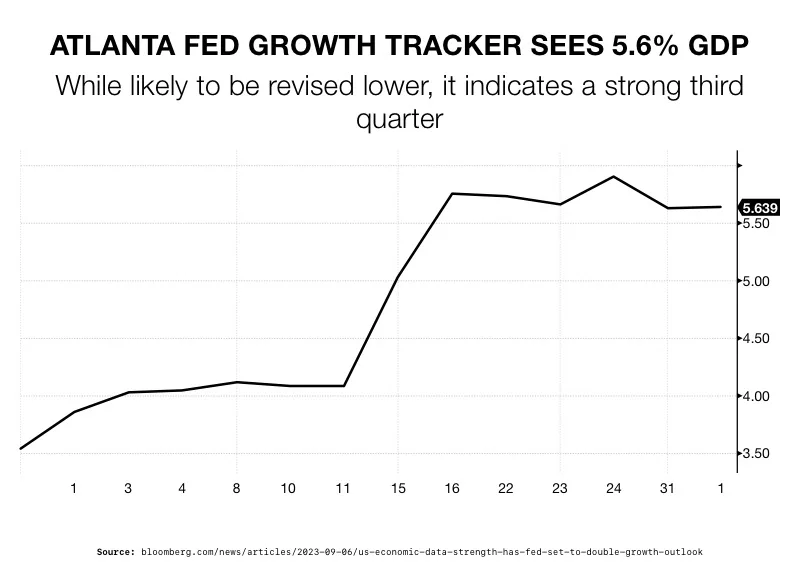

Another indicator of the Fed’s policy not working is that the GDP is growing too fast. The third quarter of 2023 far exceeded the 20-year annual average for growth. Economists attribute the GDP growth to robust consumer spending and $1 trillion of government spending on infrastructure, green energy, and the semiconductor supply chain. Also, the sudden AI boom caused an S&P 500 rally that largely reversed the Fed’s tightening of financial conditions. Even if growth slows in the fourth quarter, it may not be enough to push inflation lower.3

These factors are leading analysts to think that the neutral rate Powell is aiming for may be higher than planned. The “neutral rate” refers to the level at which the interest rate neither stimulates nor restricts economic growth. It is often considered the ideal or balanced interest rate for the economy.

No Soft Landing

Economists have compared the Fed’s quest for a soft landing to a unicorn hunt. At this time, the Fed hopes that holding rates steady will result in 2% inflation without a recession. Historically, soft landings are almost as rare as unicorns. Only once, in 1994, has the Fed accomplished a soft landing. But the inflation it tamed was hardly comparable to the recent record heights.

The Fed is playing a dangerous balancing act. If rates aren’t high enough to push inflation down to 2%, inflation expectations could rise. When people expect prices to rise, they might buy things sooner, thinking it will cost more later. This can lead to higher demand for products and services, which, in turn, can increase prices. All the accomplishments of previous rate hikes could be undone. The Fed could be forced to return with more drastic rate hikes.

Unfortunately, it may take a severe recession to reach the 2% goal. In the 1980s, then Fed Chair Paul Volcker had to inflict a recession on the US to break the rampant inflation of the 1970s. Powell is amply aware of the history. Nonetheless, he may be repeating it.

Future Hikes

Fed Chair Powell is open to more rate hikes in the future. The Federal Reserve will keep the possibility open until all signs point to a steady path to 2% inflation. The problem is that the rate of inflation is growing chaotic. It slows, then speeds up and then slows again. When the stock market believes the Federal Reserve is done increasing interest rates, financial conditions get easier. This fuels more growth, and more inflation, so the Fed must consider another rate hike. Powell outright dismissed any talk of rate cuts soon.

It’s like the Fed is driving a car on a winding road with unpredictable weather. The Federal Reserve needs to adjust its speed and direction as the road conditions change, even though they don’t control the weather. They have an idea where they want to go, they just don’t have a clear vision to get there. And if they aren’t careful, they can steer right off a cliff.

According to some analysts, we are facing more than the risk of recession, we are facing the NEED for recession. Otherwise, the economy will be trapped in this endless up and down inflationary cycle. Whether its inflation or recession, things are going to need to get worse before they get better. If you are looking to protect your savings, now is the time to investigate a Gold IRA from American Hartford Gold. Contact us today at 800-462-0071 to learn more.

2

2

4

4

2

2

5

5