- Gold broke another all-time high, hitting $2,571 an ounce

- Demand is likely to increase due to Fed rate cuts, a weaker dollar, and geopolitical uncertainty

- Buying gold now in a tax advantaged Gold IRA can lead to long-term gains

Gold Breaks New All-Time-High

Gold has been on an impressive run since the end of 2022, and it shows no signs of slowing down. On August 20th, gold reached yet another record high. Currently, gold is outperforming stocks, bonds, and even Bitcoin. Now entering its 25th year of a bull market, analysts believe that gold’s upward trend is far from over. The continuing surge is driven by a mix of global demand and economic factors.1

For the first time ever, the value of a single gold bar has crossed the $1 million mark. Of course, that single gold bar is the 400 troy ounce London Good Delivery bar. The bar is the standard unit of trade in major international gold markets. The price of gold is up more than 20% this year, trading at a record high above $2,500 an ounce, with a peak of $2,571.2

.

3

3

Gold Demand Sources

The demand for gold is global, but the reasons for this surge vary. In India, there’s a significant increase in demand due to traditional holiday buying and a recent cut in import duties. The chief executive of the London Bullion Market Association said, “It’s really a question of how quickly they can get metal into the country, in terms of the number of flights.”4

De-dollarization

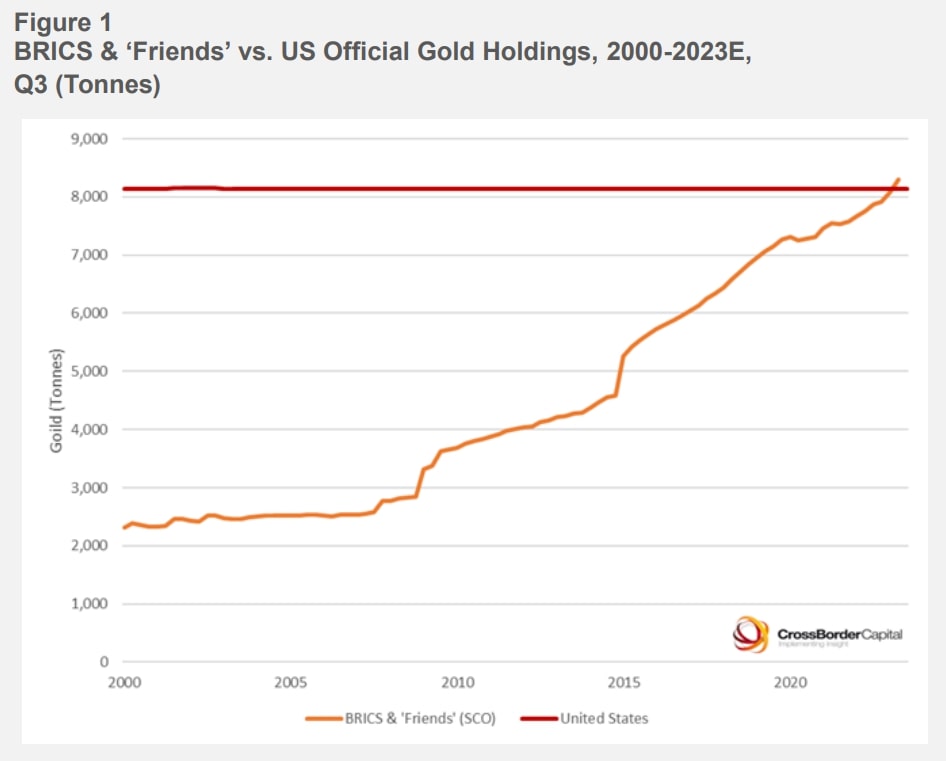

Meanwhile, demand also increased on an accelerating de-dollarization movement. The BRICS+ nations are increasing their gold reserves as they reduce their dollar holdings. They are also developing a gold-backed currency to challenge dollar supremacy. Central banks, especially the People’s Bank of China, continue to make record gold purchases. Soaring prices over the past two years have largely been fueled by China.

Geopolitics and Interest Rates

Americans are also contributing to demand. Dangerous geopolitical conflicts and the upcoming presidential election are increasing the desire for financial stability. Gold is considered a safe-haven asset, retaining its value during times of uncertainty. John Reade, chief market strategist at the World Gold Council, commented. He said, “What we have seen is investors and speculators in the West starting to return to the gold market. This has been fast money that has been driving gold.”5

Interest rates are also playing a crucial role in the gold market. Western investors largely sat on the sidelines during gold’s 20-month rally. They are now returning with the prospect of interest rate cuts. Institutional investors and bullish hedge funds are boosting gold prices. As are opaque purchases by family offices who are concerned about a devalued dollar.

Investors are betting that further interest rate cuts by the Federal Reserve will push gold prices even higher. Gold tends to rise when interest rates go down. Lower rates reduce the opportunity cost of holding non-yielding assets like gold. This makes it more attractive to investors. In addition, gold is internationally denominated in dollars. So, when the dollar goes down, gold costs more.

National Debt

However, safe haven demand isn’t just being driven by geopolitics and monetary policy. The U.S. national debt is now at $35 trillion and growing. It is eroding confidence in the dollar’s value and the creditworthiness of the United States. Investors are looking for security beyond once bedrock-solid T-bills.

Future Forecasts

Looking ahead, the gold rally appears far from over. Commerzbank expects gold prices to consolidate within the $2,500 range over the next few months. But they don’t expect them to stay static. “We expect the gold price to continue rising in the first half of 2025 due to further Fed interest rate cuts, a U.S. inflation rate that remains above target, and a weaker U.S. dollar,” said the bank’s precious metals analysts. The head of commodities at Citi Research believes that gold could reach $3,000 an ounce by mid-2025.6

Conclusion

The bottom line is that gold’s trend remains bullish as we move into September 2024. Even though aggressive bull markets rarely move in straight lines, the quarter-of-a-century trend in gold suggests that any dip could be a chance to add more gold to a diversified portfolio. Since 1999, buying every dip in gold has proven to be a strategy that yields positive returns. Those returns are amplified in a tax-advantaged Gold IRA. To learn more about how you can benefit from gold’s ascent, contact us today at 800-462-0071.

2

2

5

5

3

3

{kind=link}